1 day ago

6

1 day ago

6

ARTICLE AD BOX

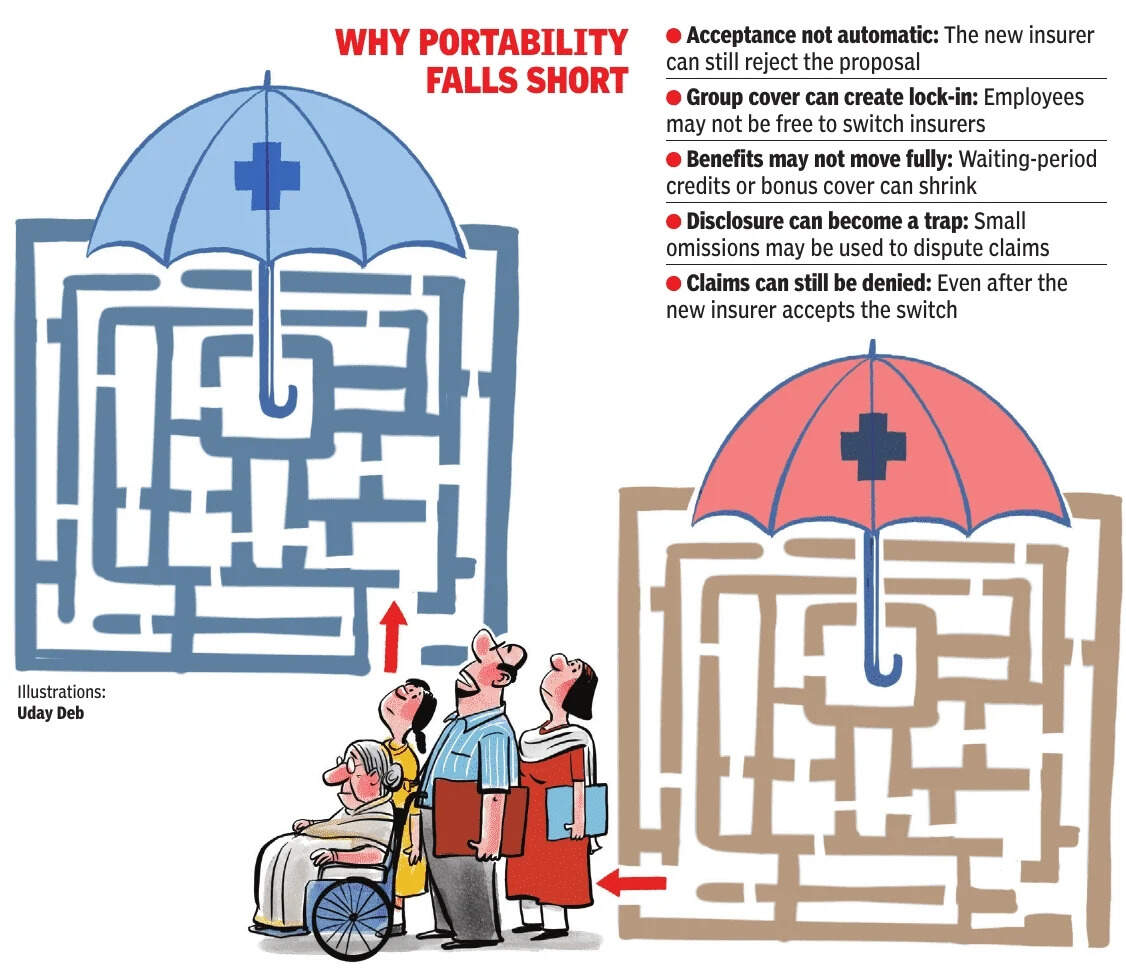

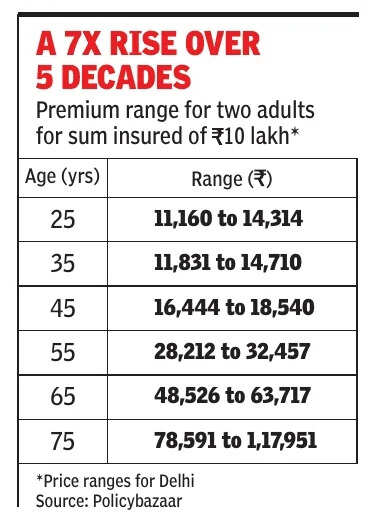

Rules were designed to preserve continuity when policyholders change cover. In practice, medical screening, limits on benefit transfers and post-claim disputes can turn what should be a straightforward move into a fraught exercise, writes Mayur ShettyHealth insurance portability was meant to let policyholders switch insurers without losing continuity benefits such as credit for waiting periods already served.

On paper, it was a major consumer reform. In reality, many policyholders find that changing insurers is still far harder than it sounds. Health insurance may be renewed every year, but a person’s medical history follows them for life. Age, illness or past claims can make a new insurer reluctant to take a customer on.Portability was introduced in 2011 to address exactly this problem. Before that, anyone who changed insurers usually had to start afresh, with waiting periods beginning again.

The new rules were meant to allow policyholders to move without automatically losing continuity benefits.But the promise of portability has often run into the reality of underwriting, product restrictions and post-claim disputes.Why switching is still difficultThe biggest surprise for many policyholders is that portability does not mean automatic acceptance. The new insurer still underwrites the proposal, reassessing the applicant’s health risk before deciding whether to issue the policy.

Long years of uninterrupted coverage do not guarantee acceptance. A claim-free record does not guarantee acceptance either. Older applicants, especially those above 50, often face greater scrutiny. So do those found to have conditions such as diabetes, hypertension or thyroid disorders during medical tests. A history of claims can also weaken the case.The problem is sharper for employees covered under group insurance policies.

Many assume that when they leave a job, they can simply move to another insurer while carrying forward the benefits built up under the employer’s cover. In practice, that is not always possible. In many cases, they can only migrate to another product offered by the same insurer rather than freely port to a different insurer of their choice.

That creates a serious lock-in.Timing is another trap. Many policyholders do not realise that portability is a process, not a last-minute formality.

The proposal should ideally go in 45 to 60 days before renewal so that the new insurance provider has time to assess the risk and communicate its decision before the old policy expires.

Then there is the issue of the no-claim bonus (NCB). Many policyholders assume that the extra cover accumulated over the years will move with them in full. Often it does not. The benefit may be tied to the product design, and a shift to another plan can reduce or reset it, leaving the customer with lower effective cover than anticipated.According to Siddharth Singhal, head of health insurance at Policybazaar, porting helps carry forward the waiting period already served but does not necessarily preserve all coverage terms because the receiving insurer underwrites the risk afresh. Policyholders, he says, must disclose all past and newly developed illnesses and avoid porting when a claim is imminent. He also says policyholders should review their cover and sum insured regularly, because continuity may apply only to the old lower sum insured when they move to a newer product.Even continuity of waiting periods, one of portability’s core promises, can become contentious. Regulations require insurers to carry forward credit for waiting periods already served for pre-existing diseases. But in practice, this can hinge on disclosure and reassessment. If the new insurer later claims that some part of the medical history was not fully disclosed, it may seek to reimpose waiting periods or dispute a claim.Real test comes at claim stage There have been cases where insurers accepted the portability request, collected the premium, and later rejected claims on grounds such as alleged non-disclosure of minor ailments or disputes over whether a treatment was medically necessary. For customers, this defeats the purpose of portability. If the insurer had concerns about the medical history, it should have examined them before accepting the policy, not after a hospitalisation claim arrives.Courts and consumer forums have increasingly taken that view.In Manjula Joisar vs Care Health Insurance, the Bombay high court upheld an ombudsman’s order directing the insurer to honour a Rs 17.8 lakh claim rejected on grounds of non-disclosure. The court held that portability is a migration of policy, not a fresh contract, and that the insurer must do its due diligence before accepting the switch.In Prakash Mehta vs Care Health Insurance, the same court held that if pre-existing conditions were known, or could have been verified, at the time of porting, they could not later be used to repudiate the claim, and directed the insurer to pay the claim with interest.Consumer forums across the country have echoed the same principle. They have generally frowned upon insurers relying on technical discrepancies, minor omissions or internal lapses after accepting portability and issuing the policy. The burden of checking medical history and past claims lies with the new insurer when it accepts the porting request.

That legal trend offers some protection to policyholders. But it also highlights the gap between the intent of portability and the experience on the ground.

If customers must go to an ombudsman, consumer forum or court to enforce continuity, the system is plainly not working as smoothly as it should.Before you switch, you must…For anyone planning to port a policy, the first rule is not to wait till the last minute. The process should begin 45 to 60 days before renewal, so there is enough time for underwriting and for the new insurer to issue a decision.The second rule is equally important: never let the existing policy lapse before the new one is formally issued.

A break in cover can wipe out the continuity benefits the policyholder is trying to preserve.Full disclosure is essential. Policyholders should disclose their complete medical history, including past consultations, tests, treatments and seemingly minor ailments. What appears trivial while filling the form can later become the basis for a disputed claim.It is also wise to seek clarity in writing on what exactly will be carried forward, particularly waiting-period credits and the treatment of the no-claim bonus.

Customers often assume portability preserves everything. In reality, what carries over may depend on the insurer and the product.The biggest mistake is to treat portability as a guaranteed right to acceptance. It is not. The right is to apply and seek continuity benefits. The new insurer still decides whether it wants to underwrite the risk.Is a second policy worth it?The portability issue also raises a broader question for salaried employees: if employer-provided cover can become uncertain after a job change, is it worth maintaining a second individual policy alongside it? In many cases, the answer may be yes. A personal policy gives continuity independent of employment and reduces the risk of being left uninsured after resigning, changing jobs or retiring.

It can also provide a fallback if the group cover is limited or the service experience is poor.There is also a regulatory reason why a second policy can be more useful than many people assume. Since 2013, policyholders have had greater flexibility in choosing which insurer to claim from when they hold more than one health policy. Instead of claims being compulsorily split proportionately between insurers, the insured can claim the full amount from one insurer of choice, up to that policy’s sum insured.That said, a second base policy is not always the cheapest way to increase cover. A top-up policy is often more affordable and may be a better option for those looking for additional protection beyond a threshold. Some advisers also suggest keeping a dedicated health fund for out-of-pocket medical expenses. But that should be seen as a supplement, not a substitute, for insurance.Portability remains an important consumer right. But it is not frictionless. It gives policyholders a route to move without automatically losing continuity benefits, yet it does not eliminate underwriting, product limitations or claim disputes. For consumers, the lesson is simple: start early, disclose everything, get the terms clarified in writing, and do not let the old cover lapse until the new one is securely in place.

English (US) ·

English (US) ·