1 hour ago

8

1 hour ago

8

ARTICLE AD BOX

MUMBAI: Corporate India is bracing for margin pressure in its fourth-quarter earnings as the escalating conflict in West Asia drives up energy prices, raising input costs for companies heavily reliant on crude oil and natural gas, and stoking broader inflation.

Sectors such as aviation, fertilizers, chemicals, paints, tyres, ceramics, logistics and glass face heightened volatility in both revenues and profitability as global energy markets tighten."Corporates with backward linkages, strategic inventory and hedging capabilities will weather the storm better than others," said Miren Lodha, senior director at Crisil Intelligence.However, the immediate impact may remain contained in the March quarter as companies are still drawing from existing inventories and hedged positions.

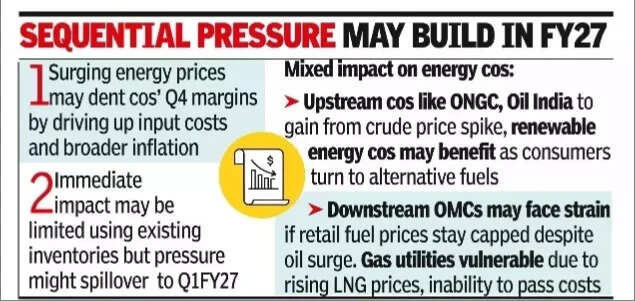

"Given just one month of conflict-related supply constraints and existing raw material, price hedges, work-in-progress, and finished goods inventory in the system, Q4 impact will be limited. The real pressure will build through fiscal 2027 as inventory cycles deplete and replacement costs rise," said Lodha.

But the pressure could intensify in the coming fiscal year as companies begin purchasing inputs at higher prices.

Crisil has projected "a decline of 40-60 basis points in the operating profit margins for corporate India in FY 2027 relative to FY 2026."The surge in energy prices compounds existing pressures from higher metal costs. "Base metals like copper, aluminium, etc. had already shot up earlier and now crude oil is moving up. Most daily items of use have some or the other derivative of crude going into it. A rally in crude prices will increase input costs of most of these companies."

said Apurva Sheth, head of market perspectives and research at Samco Securities.

which were already facing margin pressure because of the rise in the prices of base metals," The knock-on effect could extend beyond production costs in Q4. "A rally in crude oil prices is likely to stoke inflation, which is going to have an impact on the purchasing power of consumers. Higher inflation also means that the RBI will hold on to rates for longer or, maybe, it might even be forced to hike rates.

This will lead to increased interest costs for corporates," Sheth added. "Thus, if this oil shock lasts longer than expected, then it is going to have a cascading effect on the fourth-quarter performance of India Inc.

"Energy costs comprise over 20% of input costs for companies in fertilizer, paints, tyres, ceramics and glass sectors. Since most manufacturers, like those in paints and tyres, operate with 60-90 day inventory cycles, the full impact may not yet be visible in the Q4 numbers.

"Given typical 60-90 day inventory cycles, "Q4FY26 margins will be modestly better year-on-year, but sequential pressure is real. The full crude spike impact will bleed into Q1FY27, which faces a materially tougher raw material environment unless the Hormuz disruption gets resolved quickly," Sheth added.

Energy companies present a mixed picture. "Upstream companies like ONGC and Oil India benefit from the crude price spike in March, helping offset a quieter Jan-Feb period," said Sheth. Downstream oil marketing companies (OMCs) may face pressure if retail fuel prices remain capped despite higher crude costs, while gas utilities are particularly vulnerable due to rising LNG prices. and limited ability to pass on costs.Govt has approved compensation of Rs 30,000 crore for LPG under-recoveries at OMCs, but further spikes in crude prices could expand the burden. "Renewable energy companies may benefit from higher crude prices as consumers find alternatives to fossil fuels," said Sheth.

English (US) ·

English (US) ·